Pour Point Depressant Market Surges Toward USD 3.78 Billion by 2035 as Cold-Flow Efficiency Becomes Critical Across Automotive and Energy Industries

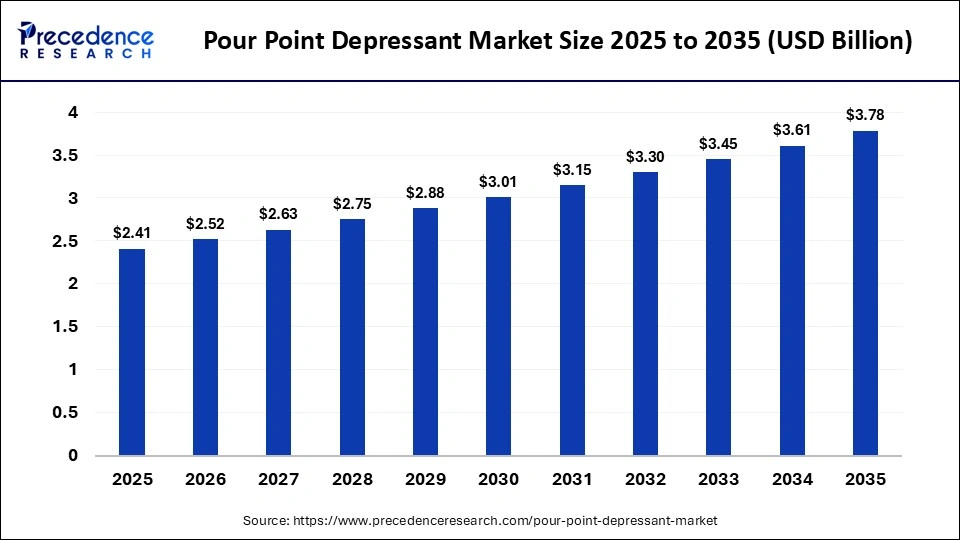

The global pour point depressant market size was valued at USD 2.41 billion in 2025 and is projected to rise from USD 2.52 billion in 2026 to nearly USD 3.78 billion by 2035, expanding at a CAGR of 4.61% from 2026 to 2035.

The increasing demand for advanced lubricants and fuel additives across automotive, oil & gas, marine, and industrial sectors is emerging as a primary catalyst behind market growth. Pour point depressants (PPDs) are becoming indispensable for maintaining the smooth flow of fuels, lubricants, and crude oil under extremely cold operating conditions. As energy transportation networks expand and industrial systems become more performance-oriented, manufacturers are investing heavily in innovative additive chemistries capable of improving wax crystal control and low-temperature fluidity.

Growing investments in refining infrastructure, offshore drilling activities, and transportation pipelines are further accelerating adoption. Additionally, stricter environmental and fuel-performance standards are pushing lubricant manufacturers toward highly efficient and sustainable additive technologies.

Pour Point Depressant Market Key Points

- The global pour point depressant market reached USD 2.41 billion in 2025 and is expected to hit USD 3.78 billion by 2035, reflecting steady industrial demand and lubricant modernization trends.

- Asia Pacific dominated the global market in 2025 with a 38% revenue share due to strong automotive manufacturing, industrialization, and energy infrastructure expansion across China and India.

- North America is projected to witness the fastest CAGR through 2035, driven by advanced pipeline technologies, stringent fuel standards, and rising investments in energy-efficient operations.

- The poly alkyl methacrylate (PAMA) segment accounted for 46.2% of the market share in 2025 owing to its superior wax crystal modification properties and broad lubricant compatibility.

- The oil & gas industry contributed 43.5% of total market revenue in 2025 because of extensive use of PPDs in crude oil extraction, storage, and transportation systems.

- Lubricants remained the leading application segment with a 52.4% share in 2025, supported by growing demand for high-performance engine oils and industrial lubricants.

- Liquid formulations dominated the market with a 68.5% share due to their superior blendability, operational convenience, and efficient dosing characteristics.

Pour Point Depressant Market Key Metrics

| Market Metrics | Details |

|---|---|

| Market Size 2025 | USD 2.41 Billion |

| Market Size 2026 | USD 2.52 Billion |

| Projected Market Size 2035 | USD 3.78 Billion |

| CAGR (2026-2035) | 4.61% |

| Leading Region | Asia Pacific |

| Fastest Growing Region | North America |

| Leading Chemistry Segment | Poly Alkyl Methacrylate (PAMA) |

| Leading End-use Industry | Oil & Gas |

| Major Application | Lubricants |

Why is the Pour Point Depressant Market Growing Rapidly?

The market is expanding steadily because industries are increasingly dependent on fuels and lubricants that remain operational under low-temperature conditions. In colder climates, hydrocarbon fluids naturally form wax crystals that reduce fluidity and disrupt transportation or machinery performance. Pour point depressants address this challenge by preventing wax crystal networking and lowering the temperature at which fluids stop flowing.

The automotive industry remains one of the strongest growth contributors due to increasing global vehicle production and rising demand for advanced engine oils and transmission fluids. Simultaneously, the oil & gas sector continues to rely heavily on PPDs for maintaining uninterrupted crude transportation through pipelines operating in harsh climates.

Industrial expansion across emerging economies is also supporting market penetration. Manufacturing facilities, heavy equipment operators, marine fleets, and mining industries are increasingly adopting premium lubricant technologies to minimize downtime and enhance machinery lifespan.

How is Artificial Intelligence Transforming the Pour Point Depressant Market?

Artificial intelligence is becoming a transformative force in the development of next-generation pour point depressants. Manufacturers are increasingly leveraging AI-powered predictive analytics and formulation modeling tools to accelerate product development cycles and reduce expensive trial-and-error experimentation.

AI platforms can simulate wax crystallization behavior, optimize additive compositions, and predict lubricant performance across varying climatic conditions. This allows chemical companies to create highly customized formulations tailored for specific base oils, fuel compositions, and industrial applications.

In addition, AI-driven manufacturing optimization is improving operational efficiency across lubricant production facilities. Predictive maintenance systems, automated quality monitoring, and intelligent process control are helping manufacturers reduce waste, improve consistency, and lower overall production costs.

Could Bio-Based Additives Become the Next Big Opportunity in the Market?

The growing shift toward environmentally sustainable industrial chemicals is creating major opportunities for bio-based pour point depressants. Governments and regulatory agencies worldwide are encouraging the use of cleaner fuels and eco-friendly lubricant formulations, prompting manufacturers to invest in greener additive chemistries.

Bio-based PPDs are increasingly being explored for biodiesel blends, renewable fuels, and low-emission lubricant applications. These additives help companies comply with sustainability regulations while maintaining operational efficiency under cold weather conditions.

As renewable energy systems and green transportation initiatives expand globally, demand for sustainable cold-flow improvers is expected to accelerate significantly over the next decade.

Can Specialized Industrial Applications Unlock New Revenue Streams?

Specialized industrial applications are rapidly emerging as high-potential growth areas for pour point depressant manufacturers.

Industries such as marine transportation, aviation, hydraulic systems, and metalworking fluids are increasingly requiring customized additive solutions capable of delivering superior low-temperature stability and wear protection. Offshore drilling platforms and Arctic oil transportation systems also represent significant growth opportunities due to their reliance on uninterrupted fluid movement in extreme environments.

Manufacturers that develop multifunctional additives combining viscosity enhancement, corrosion protection, and pour point reduction are expected to gain a strong competitive edge in the coming years.

Pour Point Depressant Market Segment Analysis

By Chemistry

The Poly Alkyl Methacrylate (PAMA) segment captured 46.2% of the global market share in 2025 due to its exceptional ability to suppress wax crystallization in fuels and lubricants. These additives offer strong compatibility across multiple base oils and deliver consistent low-temperature performance in demanding industrial environments.

PAMA-based formulations are extensively utilized in automotive lubricants, refinery operations, and pipeline transportation systems because of their reliability and operational efficiency.

Meanwhile, the ethylene-vinyl acetate (EVA) segment is projected to register the fastest growth rate through 2035. EVA additives are gaining traction for their excellent wax modification capabilities, particularly in fuels with high paraffin content and in regions experiencing severe winter conditions.

By End-Use Industry

The oil & gas segment accounted for 43.5% of global revenue in 2025 as the industry increasingly relied on pour point depressants to maintain smooth crude oil transportation and storage operations.

PPDs play a critical role in preventing wax deposition inside pipelines and storage tanks, particularly in offshore drilling and cold-region operations. As investments in pipeline infrastructure and enhanced oil recovery technologies increase globally, demand for advanced flow assurance chemicals is expected to rise further.

The automotive segment, however, is anticipated to witness the fastest growth during the forecast period due to increasing demand for high-performance engine oils and specialized lubricants for hybrid and electric vehicles.

By Application

The lubricants segment held a dominant 52.4% market share in 2025 because modern lubricants require superior low-temperature fluidity to ensure machinery protection and engine efficiency.

Automotive manufacturers, industrial machinery operators, and marine fleets are increasingly adopting premium lubricants formulated with advanced PPD technologies to reduce wear, improve startup performance, and extend equipment life.

At the same time, the crude oil transportation and pipeline segment is forecast to expand rapidly due to increasing investments in long-distance energy transportation infrastructure.

By Formulation

Liquid pour point depressants dominated with a 68.5% market share in 2025 because they offer superior blending efficiency, precise dosing capabilities, and seamless integration into existing lubrication systems.

Their operational convenience makes them highly preferred across large-scale automotive, refinery, and industrial lubricant production facilities.

On the other hand, powder and solid formulations are gaining popularity due to lower transportation costs, longer shelf life, and suitability for remote industrial operations with limited liquid handling infrastructure.

Pour Point Depressant Market Regional Insights

Asia Pacific dominated the global pour point depressant market with a 38% revenue share in 2025. Rapid industrialization, expanding automotive manufacturing, and rising fuel consumption across China and India are major contributors to regional growth.

Increasing investments in petrochemical refining, transportation infrastructure, and domestic lubricant manufacturing are also strengthening regional market leadership.

The Asia Pacific market is projected to rise from USD 927.85 million in 2025 to approximately USD 1,455.30 million by 2035, registering a CAGR of 4.60%.

India is emerging as a high-potential market due to growing oil & gas transportation activities, increasing lubricant consumption, and expanding automobile manufacturing.

Government initiatives such as Make in India are encouraging domestic specialty chemical production and attracting investments into advanced lubricant additive manufacturing facilities.

North America is expected to witness the fastest growth rate during the forecast period due to the rapid adoption of advanced pipeline technologies and high-performance lubricants.

The region’s strict environmental regulations and emphasis on fuel efficiency are encouraging manufacturers to optimize low-temperature flow properties in oils and fuels. Strong R&D capabilities and technological innovation are also supporting market expansion.

United States continues to remain a technologically advanced hub for pour point depressant innovation. Demand is being fueled by sophisticated refining infrastructure, growing industrial lubricant applications, and rising adoption of premium engine oils.

Pour Point Depressant Market Value Chain Analysis

Pour Point Depressant Market Competitive Landscape

- Afton Chemical

- BASF SE

- Chevron Phillips Chemical Company LLC

- Clariant

- Croda International Plc

- Evonik Industries AG

- Infineum International Limited

- Innospec Inc.

- The Lubrizol Corporation

- Dow Inc.

- LANXESS AG

- Solvay S.A.

- TotalEnergies

Latest Industry Development

In August 2025, Afton Chemical launched its HiTEC 65522 gasoline performance additive series designed specifically for modern Gasoline Direct Injection (GDI) engines. The new additive platform complies with the updated TOP TIER+ standard and strengthens the company’s position in advanced fuel performance technologies.

Segments Covered in the Report

By Chemistry

- Poly Alkyl Methacrylates (PAMA)

- Ethylene-Vinyl Acetate (EVA)

- Others (Styrene Esters, Poly Alpha Olefins)

By End-Use Industry

- Oil & Gas (Upstream/Midstream)

- Automotive

- Industrial Machinery

- Others (Aviation, Marine)

By Application

- Lubricants (Engine & Industrial)

- Crude Oil Transportation & Pipeline

- Fuel Blending (Diesel/Biofuels)

By Formulation

- Liquid

- Powder/Solid

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Read Also: Povidone Iodine Market Size to Surpass USD 2.59 Billion by 2035

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @https://www.precedenceresearch.com/sample/7570

You can place an order or ask any questions, please feel free to contact us at sales@precedenceresearch.com |+1 804 441 9344