Recarbonization in Chemicals Market Surges Toward $50.66 Billion by 2035 Amid Global Decarbonization Push

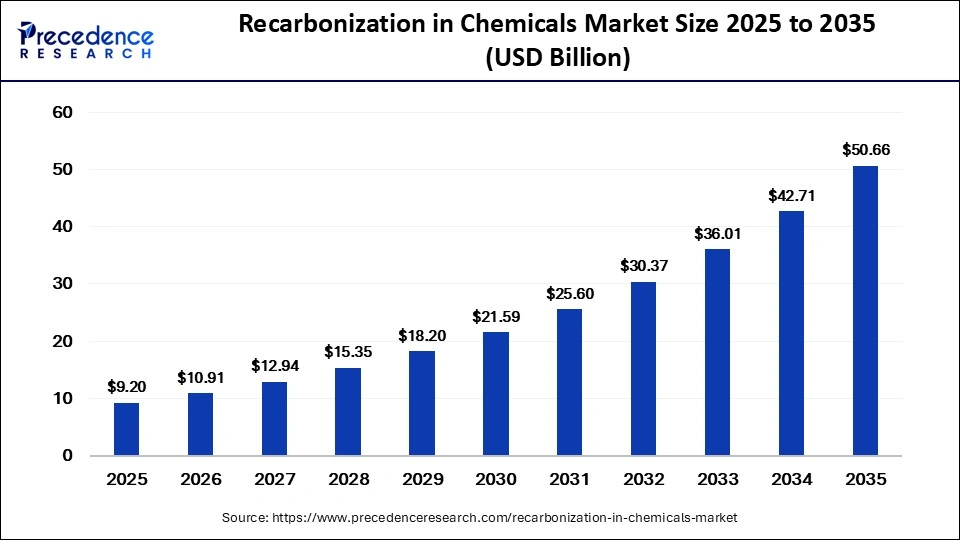

The global recarbonization in chemicals market size is projected to rise from USD 10.91 billion in 2026 to USD 50.66 billion by 2035, expanding at a compelling CAGR of 18.60%. This rapid expansion is fueled by intensifying climate regulations, net-zero commitments, and the growing shift toward sustainable chemical production using captured carbon as a valuable feedstock.

Industries worldwide are reimagining carbon not as waste but as a resource. From methanol production to synthetic fuels and polymers, recarbonization is becoming a cornerstone of the global decarbonization strategy.

Recarbonization in Chemicals Market Key Highlights

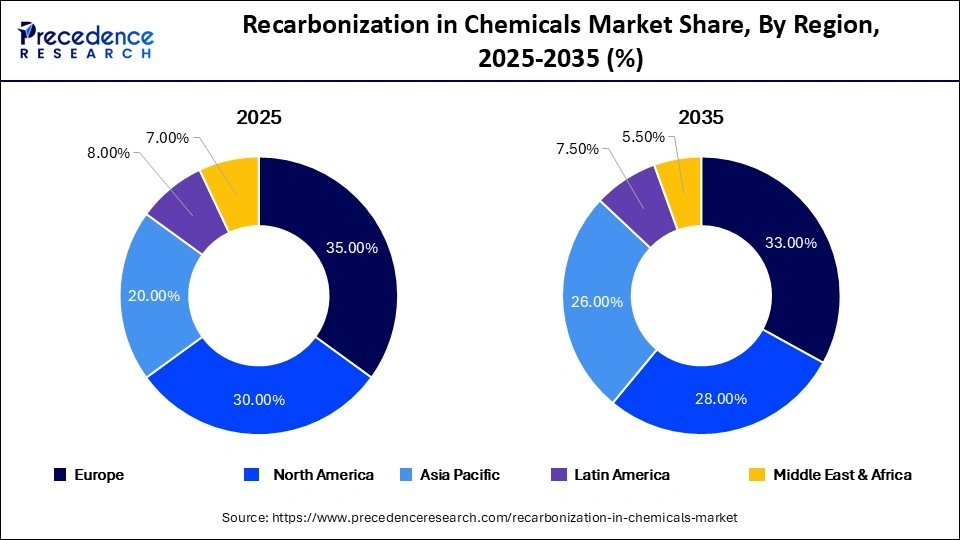

- Europe dominated the market with a 35% share, driven by strict environmental regulations.

- Asia Pacific is the fastest-growing region, expected to expand at a 21.5% CAGR through 2035.

- Carbon Capture and Utilization (CCU) led the technology segment with a 40% share in 2025.

- Methanol production emerged as the top application, accounting for 25% of total revenue.

- Industrial point sources contributed 50% share, making them the leading carbon source.

- The chemical manufacturing sector led end-use industries with a 35% share in 2025.

Artificial intelligence is playing a pivotal role in optimizing recarbonization processes. By analyzing massive datasets, AI helps improve carbon capture efficiency, refine reaction pathways, and significantly reduce energy consumption across chemical production systems.

Additionally, AI-driven predictive maintenance and real-time monitoring are enabling companies to enhance operational efficiency and reduce downtime. As scalability and cost efficiency become critical, AI is accelerating the commercialization and adoption of recarbonization technologies globally.

Recarbonization in Chemicals Market Key Growth Drivers

The market is witnessing strong growth due to a combination of regulatory, technological, and industrial factors:

- Stringent environmental regulations pushing industries toward carbon-neutral production

- Rising demand for green chemicals and low-emission fuels

- Increased investments in carbon capture technologies (CCU, CCS, DAC)

- Corporate net-zero commitments across energy, chemicals, and manufacturing sectors

- Advancements in green hydrogen and renewable feedstocks

Recarbonization in Chemicals Market Opportunities and Trends

Carbon Capture and Utilization (CCU) is enabling industries to convert CO₂ into valuable products such as methanol, polymers, and fertilizers transforming emissions into profitable assets.

Green hydrogen is emerging as a clean input for chemical processes, replacing fossil-based feedstocks and supporting low-carbon production pathways.

Digital twins, AI, and advanced analytics are optimizing production efficiency, reducing emissions, and improving real-time decision-making.

Recarbonization in Chemicals Market Key Metrics

| Report Coverage | Details |

| Market Size in 2025 | USD 9.20 Billion |

| Market Size in 2026 | USD 10.91 Billion |

| Market Size by 2035 | USD 50.66 Billion |

| Market Growth Rate from 2026 to 2035 | CAGR of 18.60% |

| Dominating Region | Europe |

| Fastest Growing Region | Asia Pacific |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Segments Covered | Technology, Application, Carbon Source, End-Use Industry, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Recarbonization in Chemicals Market Segment Analysis

Technology Insights

- CCU dominated with 40% share in 2025, driven by its ability to convert CO₂ into usable products

- DAC is the fastest-growing segment (24% CAGR) due to its atmospheric carbon removal capabilities

- CCS and carbon mineralization continue to support large-scale storage and industrial applications

Application Insights

- Methanol production accounted for 25% share, owing to its versatility as fuel and feedstock

- Synthetic fuels (e-fuels) are gaining traction with 23.5% CAGR, especially in aviation

- Growing demand for sustainable plastics and fertilizers is boosting polymer and urea segments

Carbon Source Insights

- Industrial point sources dominated (50%), offering cost-effective capture

- Direct air capture is fastest-growing, driven by carbon removal goals

- Biogenic sources are gaining traction due to their renewable nature

End-Use Insights

- Chemical manufacturing leads (35%), leveraging CO₂ as feedstock

- Energy & fuels sector is fastest-growing (21% CAGR) due to e-fuels demand

- Construction and agriculture sectors are adopting CO₂-based materials and fertilizers

Recarbonization in Chemicals Market Regional Analysis

Europe held the largest share due to strong policy frameworks like the EU Green Deal, significant investments, and early adoption of carbon capture technologies. Countries such as Germany, France, and the Netherlands are leading innovation.

North America accounted for nearly 30% share, supported by advanced infrastructure, strong R&D investments, and policy backing especially in the U.S.

Asia Pacific is emerging as the fastest-growing region due to rapid industrialization, rising emissions, and strong government initiatives in countries like China and India.

Recarbonization in Chemicals Market Key Players

Linde plc

- Supplies low‑carbon gases (oxygen, nitrogen, argon, CO₂) produced via renewable energy and low‑carbon hydrogen, enabling customers to reduce carbon intensity of chemical processes.

- Offers on‑site and merchant‑scale industrial gas plants integrated with low‑carbon hydrogen and oxy‑fuel combustion to decarbonize refineries and chemicals‑sector furnaces.

Air Liquide S.A.

- Provides low‑carbon hydrogen and CO₂ solutions, including Cryocap™ FG for capturing CO₂ from industrial flue gas and autothermal reforming / ammonia‑cracking for low‑carbon hydrogen to feed chemical plants.

- Executes carbon‑recycling projects such as the ArcelorMittal pilot converting captured carbon from steel off‑gases into bioethanol‑type chemicals, illustrating a CCU‑to‑chemicals pathway.

ExxonMobil Corporation

- Offers “Low Carbon Hydrogen” and “Low Carbon Ammonia” products where CO₂ from production is captured and sequestered, enabling fertilizer and chemicals customers to replace higher‑carbon ammonia and hydrogen.

- In chemicals, runs chemical recycling pilots (depolymersation, pyrolysis‑based) that convert plastic waste back to molecular‑level feedstocks for new chemicals and plastics.

Shell plc (Shell Chemicals / Shell Global)

- Markets “Lower Carbon Chemical Solutions” portfolio combining renewable‑energy‑powered crackers, bio‑ and circular feedstocks (e.g., pyrolysis oil), and hydrogen‑based decarbonization of steam crackers.

- At Chemicals Park Moerdijk, Shell is building a pyrolysis oil upgrader to convert hard‑to‑recycle plastic waste into chemical‑grade feedstock and is designing hydrogen‑ and CCUS‑enabled routes to achieve net‑zero emissions by 2032.

BASF SE

- Runs Biomass Balance (BMB) and “Ccycled” product lines, where bio‑based or recycled feedstocks are allocated via mass‑balance to classic chemicals (e.g., MDI/TDI, intermediates), offering certified low‑carbon “drop‑in” polymers and intermediates”.

- Develops reduced‑Product Carbon Footprint (rPCF) products by using low‑emission feedstocks and utilities, targeting chemicals‑sector customers needing lower‑embedded‑carbon intermediates.

Dow Inc.

- Pursues net‑zero chemicals production by 2050, with interim 2030 reductions via electrified crackers, hydrogen from autothermal reformers, and efficiency upgrades (e.g., at Plaquemine, Louisiana).

- Offers bio‑based polymers and emulsions (e.g., Dow PRIMAL™ Bio‑based Acrylics) that replace fossil carbon with plant‑derived carbon in formulated chemicals and coatings.

TotalEnergies SE

- Deploys green hydrogen and CCUS to decarbonize refineries feeding petrochemicals; e.g., agreements for 500,000 t/year of green H₂ and JV‑based electrolyzers with Air Liquide to supply refineries.

- While not yet a branded “recarbonized chemicals” label, these low‑carbon hydrogen and CCS projects directly lower the carbon intensity of olefins and aromatics that feed into TotalEnergies’ chemical value chain.

Carbon Clean Solutions Ltd.

- Provides modular, solvent‑based carbon capture (CycloneCC / APBS‑CDRMax) mainly for fertilizers, refineries, and industrial chemicals sites, enabling CO₂ capture from flue gas at scale.

- Leverages captured CO₂ as feedstock in integrated plants (e.g., Tuticorin Alkali’s soda‑ash complex), turning CO₂ into alkali chemicals such as soda ash and bicarbonates, exemplifying chemicals‑sector CCU.

Climeworks AG

- Focuses on direct air capture (DAC) of CO₂, then either selling gaseous CO₂ to greenhouses, food & beverage, and renewable‑fuel producers or injecting it for permanent storage.

- In chemicals contexts, Climeworks’ output can be used as carbon feedstock for synthetic fuels, methanol, or polymers, but its commercial chemical‑applications arm is still emerging versus hard‑industrial capture.

Mitsubishi Heavy Industries, Ltd. (MHI)

- Licenses and builds KM CDR Process carbon‑capture plants for chemicals sites (e.g., ammonia/urea complexes), where CO₂ from reformer flue gas is captured and re‑used as feedstock to boost urea production.

- Through its Chemicals Solution Group, MHI also trades and promotes bio‑ and carbon‑related recycling materials, positioning itself as a technology and trading partner in low‑carbon chemical feedstocks.

Aker Carbon Capture ASA

- Designs and supplies modular post‑combustion capture plants using amine‑based solvents, targeting refineries, power‑to‑X, and chemicals‑sector boilers.

- In chemicals‑adjacent cases, captured CO₂ is used in horticulture, food & beverage, but the platform is directly applicable to chemical‑plant flue‑gas decarbonization and potential CCU to chemicals.

Svante Inc.

- Develops solid‑sorbent‑based carbon capture (Svante filters) tailored for high‑CO₂ streams (≥12%) in industrial processes, including cement and chemicals.

- Captured CO₂ can be compressed to pipeline‑grade and routed to utilization routes such as methanol, urea, or polymers, supporting chemicals‑sector recarbonization via clean‑CO₂ feedstock.

CarbonCure Technologies Inc.

- Primarily a construction materials innovator: injects captured CO₂ into fresh concrete, where it mineralizes and becomes permanently embedded, reducing cement use and net emissions.

- While not a chemicals producer, CarbonCure interfaces with the value chain by converting industrial CO₂ into a building‑materials product, effectively “recarbonizing” emissions into durable materials.

Occidental Petroleum – Oxy Low Carbon Ventures

- Oxy Low Carbon Ventures (OLCV) invests in and scales CCUS projects, including direct air capture hubs (e.g., STRATOS in Texas) and CO₂‑enhanced oil recovery and storage.

- In chemicals, OLCV’s role is to supply large‑volume, low‑carbon CO₂ streams and storage infrastructure that can be drawn upon by methanol, urea, or polymer producers aiming for CO₂‑based feedstock.

SABIC

- Launched a “certified low carbon” product portfolio, starting with methanol produced using captured CO₂ from its own operations, intended for downstream chemicals and materials.

- Aims to integrate electrification, hydrogen, and CCUS across its chemical complexes to deliver low‑carbon versions of olefins, aromatics, and base chemicals to customers.

Latest Industry Developments

- India announced ₹20,000 crore investment (2026) for CCUS expansion

- China launched a green hydrogen-based coal-to-chemicals project (2025)

- Germany introduced a €6 billion decarbonization program

- Europe commissioned a commercial-scale e-methanol plant

Segments Covered in the Report

By Technology

- Carbon Capture and Utilization (CCU)

- Carbon Capture and Storage (CCS)

- Direct Air Capture (DAC)

- Carbon Mineralization

By Application

- Methanol Production

- Urea & Fertilizers

- Polymer & Plastics Production

- Synthetic Fuels (e-fuels)

- Concrete & Building Materials

By Carbon Source

- Industrial Point Sources (Cement, Steel, Refineries)

- Biogenic Sources (Biomass, Fermentation)

- Direct Air Capture Sources

By End-Use Industry

- Chemical Manufacturing

- Energy & Fuels

- Construction Materials

- Agriculture

- Automotive & Industrial

By Region

- North America

- Latin America

- Europe

- Asia-pacific

- Middle and East Africa

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/8363

You can place an order or ask any questions, please feel free to contact us at sales@precedenceresearch.com |+1 804 441 9344