Metal Coil Lamination Market Size Forecasted to Reach USD 8.71 Billion by 2035 as Smart Manufacturing and Sustainable Coatings Accelerate Global Demand

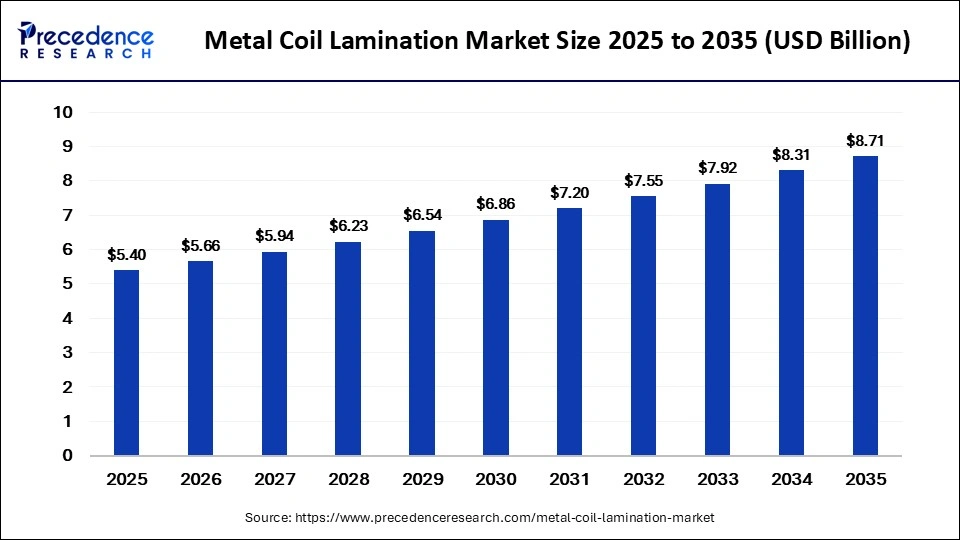

The global metal coil lamination market is witnessing strong momentum as industries increasingly prioritize durable, corrosion-resistant, and aesthetically advanced coated metal solutions. The global metal coil lamination market size was valued at USD 5.40 billion in 2025 and is projected to grow from USD 5.66 billion in 2026 to approximately USD 8.71 billion by 2035, expanding at a CAGR of 4.90% during the forecast period from 2026 to 2035.

The rapid expansion of smart infrastructure, electric vehicle manufacturing, industrial automation, and energy-efficient appliances is significantly boosting demand for laminated metal coils worldwide. Manufacturers are increasingly integrating advanced coating technologies and AI-enabled inspection systems to enhance production quality, improve operational efficiency, and reduce environmental impact.

Why is the Metal Coil Lamination Market Gaining Strong Momentum Worldwide?

Metal coil lamination has emerged as a critical process across construction, automotive, electronics, appliances, and industrial manufacturing sectors. The process involves bonding protective films and coatings onto metal coils such as steel, aluminum, and stainless steel to improve durability, appearance, flexibility, and resistance against corrosion, UV radiation, and harsh environments.

Growing urbanization, rising infrastructure investments, and the global shift toward lightweight yet durable materials are accelerating the use of laminated metal products. Industries are increasingly adopting laminated coils for roofing systems, automotive body panels, premium appliances, and packaging applications due to their improved lifespan and aesthetic appeal.

Additionally, evolving sustainability standards and strict emission regulations are encouraging manufacturers to adopt water-based and eco-friendly coating technologies, creating new opportunities for innovation in the market.

Metal Coil Lamination Market Key Points

- The global metal coil lamination market is expected to reach USD 8.71 billion by 2035 from USD 5.66 billion in 2026.

- The market is projected to expand at a CAGR of 4.90% between 2026 and 2035.

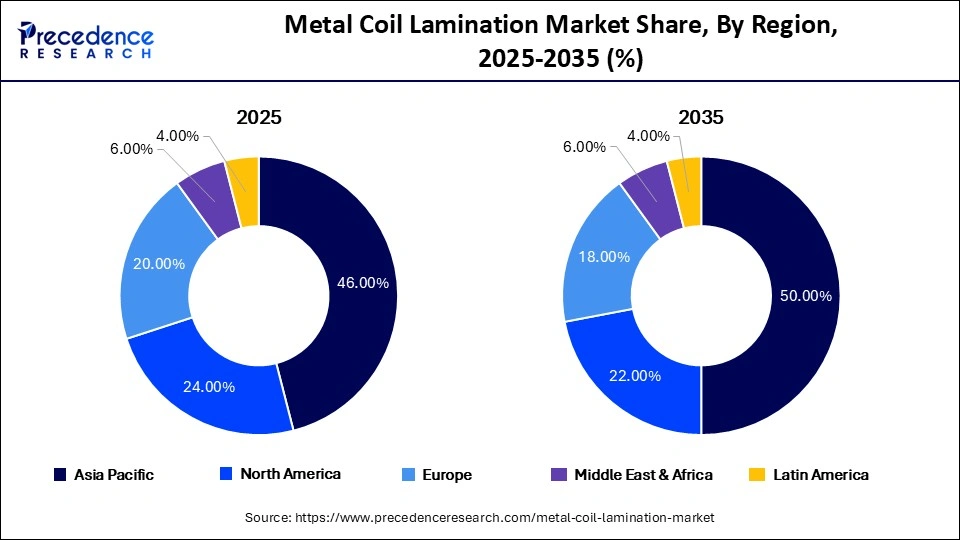

- Asia-Pacific dominated the global market with a 46% revenue share in 2025.

- Asia-Pacific is also anticipated to witness the fastest growth rate of 6.2% during the forecast period.

- Steel remained the leading material segment with a 52% market share in 2025.

- Aluminum is projected to be the fastest-growing material segment with a CAGR of 6.5%.

- Thermal lamination led the market with a 40% share in 2025.

- Extrusion lamination is expected to grow at the fastest CAGR of 5.8%.

- Polyester coating accounted for 34% of total market revenue in 2025.

- PVDF coating is forecast to grow rapidly at a CAGR of 6%.

- Building and construction emerged as the dominant application segment with 38% market share.

- Automotive applications are expected to grow strongly with a CAGR of 6.2%.

- Construction remained the largest end-use industry with 36% market share in 2025.

- The 0.3–1 mm thickness segment dominated the market with a 46% share.

How is Artificial Intelligence Transforming the Metal Coil Lamination Industry?

Artificial intelligence is becoming a game-changing force in the metal finishing and lamination ecosystem. AI-powered visual inspection systems are helping manufacturers detect coating defects with exceptional speed and precision by analyzing thousands of surface images in real time. This significantly improves product consistency while minimizing production losses.

AI-enabled predictive maintenance solutions are also helping manufacturers reduce downtime by continuously monitoring machinery performance through vibration, temperature, and pressure sensors. These intelligent systems allow operators to identify maintenance requirements before failures occur, improving plant productivity and operational reliability.

Moreover, AI is streamlining workflow optimization by ensuring proper coil sequencing, reducing wastage, and enhancing manufacturing efficiency. The integration of machine learning and industrial automation is expected to redefine quality control standards across the global metal coil lamination market over the next decade.

Metal Coil Lamination Market Size Overview

| Market Metrics | Details |

|---|---|

| Market Size in 2025 | USD 5.40 Billion |

| Market Size in 2026 | USD 5.66 Billion |

| Forecast Market Size by 2035 | USD 8.71 Billion |

| CAGR (2026–2035) | 4.90% |

| Dominating Region | Asia-Pacific |

| Fastest Growing Region | Asia-Pacific |

| Base Year | 2025 |

| Forecast Period | 2026–2035 |

What are the Major Growth Drivers Fueling the Metal Coil Lamination Market?

Increasing Demand for Durable and Lightweight Materials

The rising preference for lightweight, corrosion-resistant, and energy-efficient materials across automotive, aerospace, and construction sectors is driving strong market expansion. Laminated metal coils offer superior structural strength, thermal performance, and design flexibility, making them highly suitable for modern industrial applications.

The automotive industry, especially electric vehicle manufacturers, is increasingly adopting aluminum laminated coils to reduce vehicle weight and improve fuel efficiency. Similarly, infrastructure developers are utilizing laminated metal products in roofing, cladding, and façade systems for enhanced durability and aesthetics.

Rapid Expansion of Smart Appliance Manufacturing

The global rise in smart appliances and premium home electronics is further contributing to market growth. Manufacturers are seeking visually appealing, scratch-resistant, and high-performance coated metal surfaces that align with evolving consumer preferences.

Growing Industrial Automation

The integration of automated manufacturing processes is increasing the demand for high-precision laminated metal products. Automated production lines require consistent coating quality, improved flexibility, and superior durability, encouraging manufacturers to adopt advanced lamination technologies.

What Trends are Reshaping the Future of the Metal Coil Lamination Market?

Why are Customized Premium Finishes Becoming Popular?

Manufacturers are increasingly focusing on customized textures, decorative finishes, and color-coated laminated coils to cater to modern architectural and automotive design preferences. Export-oriented markets are especially demanding premium-quality laminated materials with enhanced aesthetics and long-lasting performance.

How are Smart and Energy-Efficient Applications Influencing Demand?

The rising popularity of smart electronics and energy-efficient infrastructure is driving the adoption of laminated metal solutions in appliance manufacturing and advanced electronic systems. These materials improve thermal efficiency while supporting sleek modern product designs.

Why are Durable Coatings Emerging as a Key Industry Trend?

Demand for anti-corrosion, UV-resistant, and heat-resistant laminated layers is growing rapidly across industrial, automotive, and construction applications. These advanced coatings significantly improve product lifespan while reducing maintenance costs.

Expert Perspective

According to the Precedence Research Principal Consultant,

“The metal coil lamination market is entering a transformative phase driven by sustainable coating technologies, AI-enabled manufacturing, and rising demand for lightweight industrial materials. Companies investing in eco-friendly laminates and high-performance coatings will gain a strong competitive edge over the coming decade.”

Metal Coil Lamination Market Segmental Analysis

Material Type Analysis

The steel segment accounted for the largest share of the metal coil lamination market, capturing 52% in 2025. Its dominance was supported by extensive use in construction and industrial manufacturing due to its strength, durability, and cost-effectiveness. Rising infrastructure projects and increasing demand for coated structural materials further strengthened market growth.

The aluminum segment held around 24% market share in 2025 and is projected to expand at the fastest CAGR of 6.5% during the forecast period. Growth is driven by increasing demand for lightweight automotive components, energy-efficient buildings, and recyclable materials. Expanding applications in transportation and appliances are also supporting segment growth.

The stainless steel segment represented nearly 16% of the market in 2025. Demand is increasing due to its superior durability and corrosion resistance, particularly in industrial, architectural, healthcare, and food processing applications. Growth in specialty manufacturing operations is further contributing to segment expansion.

The copper segment captured approximately 8% market share in 2025 and is expected to witness steady growth. Strong thermal and electrical conductivity make copper highly suitable for electrical and electronics applications. Growing precision engineering and industrial component demand are supporting market development.

Metal Coil Lamination Market Share, By Material Type, 2025-2035 (%)

| Material Type | 2025 | 2035 | CAGR (%) |

| Steel | 52.00% | 50.00% | 4.5% |

| Aluminum | 24.00% | 28.00% | 6.5% |

| Stainless Steel | 16.00% | 15.00% | 4.2% |

| Copper | 8.00% | 7.00% | 3.8% |

Lamination Type Analysis

Thermal lamination dominated the market with a 40% share in 2025. The segment benefits from cost-effective production, strong adhesion properties, and broad usage in industrial and appliance applications. Increasing demand for decorative and protective metal finishes also supported its leading position.

The adhesive lamination segment accounted for around 35% of the market in 2025 and is projected to grow steadily. Demand is rising for high-performance bonding solutions in automotive and construction industries, along with flexible laminated materials used in specialty manufacturing.

Extrusion lamination held nearly 25% market share in 2025 and is expected to grow at the fastest pace. Rising use of moisture-resistant and chemical-resistant coatings in packaging and industrial protection applications is driving demand. Technological advancements in multilayer coatings are further boosting growth.

Metal Coil Lamination Market Share, By Lamination Type, 2025-2035 (%)

| Lamination Type | 2025 | 2035 | CAGR (%) |

| Thermal Lamination | 40.00% | 38.00% | 4.4% |

| Adhesive Lamination | 35.00% | 36.00% | 5.2% |

| Extrusion Lamination | 25.00% | 26.00% | 5.8% |

Coating Type Analysis

Polyester coating led the market with approximately 34% share in 2025. The segment is widely used in roofing, cladding, and construction applications because of its affordability, weather resistance, and aesthetic appeal. Expanding commercial construction activities are supporting continued demand.

PVDF coating accounted for around 26% market share and is projected to grow at the fastest CAGR of 6%. Superior UV resistance, chemical protection, and suitability for premium architectural projects are key growth drivers. Adoption is also increasing in harsh environmental conditions.

The polyurethane coating segment secured nearly 22% market share in 2025. Its strong abrasion and corrosion resistance properties make it ideal for industrial and marine applications. Increasing demand for long-lasting protective systems continues to support market growth.

Plastisol coating represented approximately 18% of the market in 2025. The segment benefits from excellent flexibility, impact resistance, and insulation properties, particularly in automotive and industrial storage applications.

Metal Coil Lamination Market Share, By Coating Type, 2025-2035 (%)

| Coating Type | 2025 | 2035 | CAGR (%) |

| Polyester Coating | 34.00% | 32.00% | 4.5% |

| PVDF Coating | 26.00% | 28.00% | 6.0% |

| Polyurethane Coating | 22.00% | 23.00% | 5.5% |

| Plastisol Coating | 18.00% | 17.00% | 4.0% |

Application Analysis

The building and construction segment held the largest market share of 38% in 2025. Rapid urbanization, infrastructure development, and increasing demand for corrosion-resistant building materials are major growth drivers. Rising adoption of energy-efficient roofing systems also contributed to segment dominance.

The automotive segment captured around 24% of the market in 2025 and is expected to grow at the fastest CAGR of 6.2%. Rising electric vehicle production and increasing use of lightweight coated metals for durability and corrosion resistance are driving market expansion.

The appliances segment accounted for nearly 18% market share in 2025. Demand is rising for visually appealing and durable metal surfaces in household appliances, supported by growth in smart appliance manufacturing worldwide.

The packaging segment secured about 12% of the market in 2025. Growing need for moisture-resistant packaging materials and increasing adoption of sustainable packaging solutions are contributing to segment growth.

Metal Coil Lamination Market Share, By Application, 2025-2035 (%)

| Application | 2025 | 2035 | CAGR (%) |

| Building & Construction | 38.00% | 39.00% | 5.5% |

| Automotive | 24.00% | 26.00% | 6.2% |

| Appliances | 18.00% | 17.00% | 4.5% |

| Packaging | 12.00% | 11.00% | 4.0% |

| Industrial Equipment | 8.00% | 7.00% | 4.2% |

End-use Industry Analysis

The construction industry accounted for 36% of the market share in 2025. Increasing investments in residential, commercial, and industrial infrastructure projects are boosting demand for durable coated metal products and energy-efficient construction materials.

The automotive and transportation segment captured approximately 26% market share in 2025 and is projected to grow at the fastest pace. Expansion of electric vehicle manufacturing and rising use of lightweight laminated metals are key factors supporting growth.

The consumer electronics segment held around 14% market share in 2025. Rising demand for premium-finish electronic devices and growing electronics production facilities are contributing to market development.

Industrial manufacturing represented nearly 16% of the market in 2025. Increasing adoption of corrosion-resistant materials in machinery, automation systems, and factory operations is supporting segment expansion.

Metal Coil Lamination Market Share, By End-use Industry, 2025-2035 (%)

| End-use Industry | 2025 | 2035 | CAGR (%) |

| Construction | 36.00% | 37.00% | 5.5% |

| Automotive & Transportation | 26.00% | 28.00% | 6.2% |

| Consumer Electronics | 14.00% | 13.00% | 4.6% |

| Industrial Manufacturing | 16.00% | 15.00% | 4.5% |

| Packaging Industry | 8.00% | 7.00% | 4.0% |

Thickness Analysis

The 0.3–1 mm thickness segment led the market with a 46% share in 2025. Its balanced strength and flexibility make it highly suitable for automotive, construction, appliance, and industrial manufacturing applications.

The above 1 mm segment accounted for around 32% market share and is projected to grow rapidly. Rising demand for heavy-duty industrial and infrastructure applications, along with superior durability and impact resistance, are key growth drivers.

The below 0.3 mm segment secured nearly 22% market share in 2025. Increasing applications in lightweight electronics, decorative products, and appliances are contributing to segment growth.

Metal Coil Lamination Market Regional Analysis

Asia-Pacific emerged as the dominant regional market with 46% share in 2025 and is projected to witness the fastest CAGR of 6.2% throughout the forecast period.

The region benefits from strong steel and aluminum manufacturing capabilities across China, India, Japan, and South Korea. Rapid industrialization, urban infrastructure development, and growing automotive production are significantly driving market demand.

China continues to play a central role in regional growth. Major companies including Baowu Steel Group, Ansteel Group, and Shougang Group are expanding premium laminated coil production to meet rising infrastructure and housing demand.

Europe accounted for 24% of market revenue in 2025, supported by strong automotive manufacturing and rising demand for sustainable building materials.

Germany remains a key contributor due to growing adoption of AI-powered inspection systems and high-precision laminated metal technologies within the automotive sector.

North America captured 20% of the market share in 2025. Rising infrastructure modernization projects, green building initiatives, and increasing investments in advanced manufacturing facilities are driving regional demand.

The U.S. market is experiencing growing demand for customizable pre-finished laminated coils that help streamline fabrication and reduce operational costs.

What Opportunities are Emerging for Industry Participants?

The rising global focus on sustainable construction and carbon-neutral infrastructure is opening significant growth opportunities for manufacturers.

Companies are increasingly investing in low-emission, water-based, and high-solid coating technologies to comply with strict environmental regulations. These innovations are helping reduce energy consumption, improve manufacturing efficiency, and lower carbon footprints.

Furthermore, the growing adoption of smart factories and Industry 4.0 technologies is expected to create long-term opportunities for AI-driven lamination systems and automated quality inspection solutions.

Recent Industry Developments

Covestro Expands Sustainable Coating Resin Production

In September 2025, Covestro expanded production of its non-PFAS flexible powder coating polyester resins, Uralac Premium P 8000 and P 9000, across the Asia-Pacific region. The initiative strengthened the company’s sustainable coatings portfolio while addressing increasingly strict environmental regulations.

Merino Group Launches Premium Metal-Finish Laminate

In April 2025, Merino Group introduced “Metalam,” a premium decorative metal-finish laminate designed for vertical and ceiling applications in high-impact commercial environments. The product combines the visual appeal of real metal with the flexibility of decorative laminates.

Leading Companies in the Metal Coil Lamination Market

Nippon Steel

ORIENTCORE HI-B, HI-B LS, HI-B PM grain-oriented electrical steel products

CRGO thickness range: 0.15–0.35mm

Product forms: Mother coils, slit coils, laminations

Applications: Transformers, reactors, inverters

ArcelorMittal

Semi-processed standard & high permeability non-oriented electrical steel (NOES) grades

Product forms: Coils, sheets

Applications: Power generation, motors, generators

Tata Steel

Cold Rolled Coils/Sheets including Tata Steelium & Tata Steelium Neo

CRGO for transformer applications

Product forms: Coils, sheets, slit coils

Applications: Automobile, transformers, electrical components

Baosteel

CRGO mother coils, slit coils, transformer laminations (0.1–0.35mm)

B20R070 laser-scribed electrical steel

Product forms: Transformer core laminations, coils

Applications: Transformer cores, energy-efficient equipment

POSCO

PG-Core (CGO), HGO, DR grades including 23HP85, 27HP95

Ultra-thin electrical steel: 0.08–0.15mm

Product forms: Mother coil, slit coil, CTL (Continuous Transformer Lamination)

Applications: Power transformers, EV motors, reactors

JFE Steel

JFE G-CORE (grain-oriented), JFE N-CORE (non-grain-oriented)

JFE CORESTAR series with Hi-M3, Hi-B materials

Product forms: Electrical steel sheets, laser-cut laminations, JGSE CORE (50–1,050mm width)

Applications: Transformers, motor prototyping, toroidal cores

JSW Steel

Electrical Steel (ES) in coil, slit, and sheet forms

Grades for precision motors and generators

Product forms: Coil slits, sheets

Applications: Precision motors, generators

Thyssenkrupp

NO & GOES electrical steel portfolio

bluemint® grades with up to 50% CO₂ reduction

Product forms: Blanks (0.4–16mm), electrical steel strip

Applications: Power grid decarbonization, transformers

Voestalpine

isovac® HPNO grades (0.25–0.27mm thickness, >1300mm width)

Y420 premium strength grade for drive motors

Product forms: Electrical steel strip, coils

Applications: E-mobility drive motors, generators, transformers

Novelis

Laminated aluminum coil surfaces with black laminating film

Product forms: Laminated aluminum coils

Applications: Beverage can ends (packaging segment, not electrical steel)

U.S. Steel

CRML Grades 1–9 (cold-rolled motor lamination steel)

Only two North American mills producing all 9 CRML grades

Non-oriented (NGO) steel, one of thinnest/widest electrical steel

Applications: Motors, generators, specialty transformers, EVs

Dongkuk Steel

Pre-coated metal: Luxteel, Appsteel

Galvanized and Galvalume coils

Product forms: Pre-coated metal, galvanized coils

Applications: Home appliances, construction (limited electrical steel lamination)

BlueScope Steel

Coil coating solutions: polyester, PVDF, plastisol on HDG, Galvalume, cold-rolled coils

Product forms: Coated steel/aluminum coils

Applications: Automotive, construction, HVAC

SSAB

Electrogalvanized steels, Docol® AHSS with metal coatings

Galfan® coatings for corrosion resistance

Product forms: Metal-coated coils, plates

Applications: Automotive OEMs, energy, heavy transport

NLMK Group

NGO electrical steel (Dynamo steel): High Grades, High Frequency (for EVs), HPG grades

Product forms: Coils, sheets

Applications: Electrical motors, generators, EVs

Segments Covered in the Report

By Material Type

- Steel

- Aluminum

- Stainless Steel

- Copper

By Lamination Type

- Thermal Lamination

- Adhesive Lamination

- Extrusion Lamination

By Coating Type

- Polyester Coating

- PVDF Coating

- Polyurethane Coating

- Plastisol Coating

By Application

- Building & Construction

- Automotive

- Appliances

- Packaging

- Industrial Equipment

By End-use Industry

- Construction

- Automotive & Transportation

- Consumer Electronics

- Industrial Manufacturing

- Packaging Industry

By Thickness

- Below 0.3 mm

- 0.3–1 mm

- Above 1 m

By Region

- North America

- Latin America

- Europe

- Asia-pacific

- Middle and East Africa

Read Also: Povidone Iodine Market Size to Surpass USD 2.59 Billion by 2035

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/8409

You can place an order or ask any questions. Please feel free to contact us at sales@precedenceresearch.com |+1 804 441 9344