FRP Pipe Market Size to Surpass USD 8.99 Billion by 2035 Amid Rising Water Infrastructure and Industrial Pipeline Upgrades

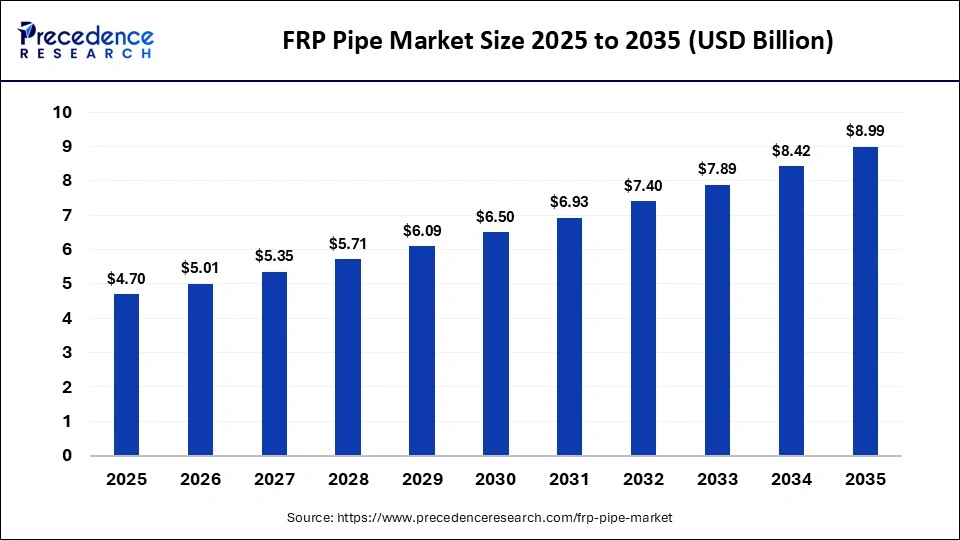

The global FRP pipe market is witnessing sustained expansion as governments, utilities, and industrial operators increasingly shift toward corrosion-resistant and low-maintenance piping systems. The market size stood at USD 4.70 billion in 2025 and is projected to rise from USD 5.01 billion in 2026 to nearly USD 8.99 billion by 2035, registering a CAGR of 6.71% between 2026 and 2035. Demand growth is being fueled by rising investments in municipal water infrastructure, growing deployment of desalination and wastewater treatment facilities, and increasing replacement of aging steel and concrete pipelines across industrial sectors.

Fiber-reinforced polymer (FRP) pipes are becoming a preferred alternative to traditional piping materials because of their high corrosion resistance, lightweight structure, superior lifecycle performance, and lower maintenance costs. Industries such as oil & gas, chemicals, mining, power generation, and municipal utilities are increasingly specifying FRP piping systems for applications exposed to aggressive chemicals, saline water, and extreme environmental conditions.

FRP Pipe Market Key Points

- The global FRP pipe market was valued at USD 4.70 billion in 2025 and is expected to reach USD 8.99 billion by 2035.

- The market is anticipated to grow at a CAGR of 6.71% from 2026 to 2035.

- North America dominated the market in 2025 with a 40.4% market share due to extensive infrastructure rehabilitation projects.

- Asia Pacific is expected to witness the fastest growth during the forecast period with a CAGR of 6%.

- Polyester FRP pipes led the material segment with a 45.6% market share in 2025.

- Oil & gas emerged as the leading application segment, accounting for 42.3% of the global market share.

- Industrial end-users captured 40.4% of total revenue in 2025 owing to rising use in chemical processing and energy infrastructure.

- Bell-and-spigot joint systems dominated the market with a 52.4% share due to superior sealing and installation flexibility.

- Increasing investment in water supply systems, wastewater treatment, and desalination plants continues to strengthen long-term market demand.

FRP Pipe Market Revenue Snapshot

| Market Indicator | Value |

|---|---|

| Market Size 2025 | USD 4.70 Billion |

| Market Size 2026 | USD 5.01 Billion |

| Forecast Market Size 2035 | USD 8.99 Billion |

| CAGR (2026–2035) | 6.71% |

| Leading Region | North America |

| Fastest Growing Region | Asia Pacific |

Why Is the FRP Pipe Market Expanding Rapidly Across Global Industries?

The increasing failure rates of aging metallic pipelines and the rising need for corrosion-resistant infrastructure are among the primary drivers behind FRP pipe adoption worldwide. Conventional steel and concrete pipelines often deteriorate rapidly when exposed to harsh chemicals, saline water, hydrogen sulfide, and fluctuating temperatures. FRP pipes provide a highly durable alternative capable of delivering long operational life with minimal maintenance requirements.

Another major growth factor is the expansion of municipal wastewater treatment systems and industrial effluent management infrastructure. Governments worldwide are investing heavily in water conservation, sewage transport systems, and desalination facilities to address urban population growth and water scarcity challenges. FRP pipes are increasingly preferred because they reduce leakage risks, lower energy consumption, and provide superior hydraulic performance due to their smooth internal surfaces.

Industrial sectors are also accelerating demand. Chemical processing facilities, offshore oil platforms, refineries, mining operations, and power generation plants are shifting toward FRP systems because of their ability to withstand corrosive media while maintaining structural integrity under high-pressure operating environments.

How Is Artificial Intelligence Transforming the FRP Pipe Manufacturing Industry?

Artificial intelligence is significantly reshaping the FRP pipe manufacturing ecosystem by introducing predictive analytics, smart quality monitoring, and automated production optimization. AI-driven simulation tools are enabling manufacturers to model fiber orientation, resin distribution, laminate stacking, and stress behavior before physical manufacturing begins. This improves product performance while reducing raw material waste and prototyping costs.

Machine learning algorithms are also being integrated into filament winding and centrifugal casting operations to optimize winding angles, fiber tension, and resin impregnation consistency. These capabilities are helping manufacturers improve pressure ratings, enhance joint durability, and ensure batch-to-batch mechanical uniformity.

AI-powered vision inspection systems are emerging as a critical innovation in quality assurance. These systems can identify delamination, voids, dry fiber regions, and structural inconsistencies in real time using advanced imaging and sensor analytics. Manufacturers are increasingly using predictive maintenance models to monitor curing ovens, winding equipment, and automated production systems, reducing downtime while improving operational efficiency.

Could Government Infrastructure Projects Become the Biggest Opportunity for FRP Pipe Manufacturers?

Government-funded infrastructure modernization programs are expected to create massive long-term opportunities for FRP pipe manufacturers globally. Countries are upgrading water transmission systems, sewer pipelines, stormwater drainage networks, and industrial utility infrastructure to meet rising urbanization demands.

India’s National Water Mission, China’s urban infrastructure modernization initiatives, and wastewater recycling programs across the Middle East are creating strong demand for corrosion-resistant piping technologies. Since FRP pipes offer longer service life and lower lifecycle maintenance costs compared to steel and concrete, public authorities increasingly view them as a sustainable long-term investment.

The growing emphasis on reducing water leakage and improving urban water efficiency is likely to accelerate municipal adoption even further over the next decade.

Why Are Sustainable Materials Becoming a Major Trend in the FRP Pipe Industry?

Sustainability is becoming a central theme across the global construction and infrastructure sectors, and FRP pipes are benefiting from this transition. Environmental regulations increasingly encourage the use of recyclable, low-maintenance, and corrosion-resistant materials that minimize long-term environmental impact.

FRP pipes have a lower lifecycle carbon footprint due to reduced maintenance requirements and extended operational durability. Their lightweight structure also lowers transportation-related emissions and installation energy requirements. Municipalities and industrial operators are increasingly adopting FRP systems to align with environmental compliance standards and sustainability objectives.

Additionally, advancements in resin technologies and embedded monitoring systems are helping improve operational efficiency and enabling predictive infrastructure management.

FRP Pipe Market Segmental Analysis

Material/Type Analysis

The polyester FRP pipe segment accounted for the largest market share of 45.6% in 2025. Its dominance is driven by a strong balance of mechanical strength, corrosion resistance, and cost efficiency. These pipes are widely used in chemical transportation, municipal water systems, and industrial effluent applications because they can withstand moderate pressure and temperature conditions effectively.

Polyester FRP pipes are also preferred for large infrastructure projects due to their simple manufacturing process, easy raw material availability, and suitability for large-diameter installations.

The polyurethane pipe segment is projected to grow at the fastest CAGR of 5.4% during the forecast period. Rising demand for flexible, abrasion-resistant, and impact-resistant piping solutions is driving adoption across mining slurry transport and harsh industrial environments.

These pipes provide excellent structural integrity under dynamic loading conditions, making them suitable for energy projects and heavy industrial operations.

Application Analysis

The oil & gas industry remains the leading application segment for FRP pipes due to the growing need for lightweight and corrosion-resistant piping systems. FRP pipes are extensively used in produced water systems, chemical injection systems, and firewater networks.

Their resistance to corrosive gases, saltwater, and chemicals reduces long-term maintenance costs, making them ideal for hydrocarbon transportation and offshore operations.

The water & wastewater segment is expected to expand at a CAGR of 5.2% between 2026 and 2035. Increasing investments in urban water supply, sewage treatment, and desalination projects are supporting this growth.

FRP pipes are gaining popularity because of their long service life, smooth internal surfaces, and resistance to microbial and chemical corrosion. These advantages help reduce leakage, lower energy consumption, and minimize maintenance disruptions.

End-User Analysis

The industrial segment captured the largest market share of 40.4% in 2025. Industries such as chemical processing, oil refining, mining, and power generation increasingly rely on FRP pipes for handling corrosive liquids and gases.

FRP pipes offer high pressure resistance, durability, and lower lifecycle costs compared to metal pipes. Their lightweight structure also simplifies installation in complex industrial facilities.

The commercial segment is projected to grow at a CAGR of 5.2% during the forecast period. Growth is supported by rising investments in commercial infrastructure projects, data centers, and institutional buildings in emerging economies.

FRP pipes are increasingly used in HVAC systems, fire protection systems, and utility piping because they offer design flexibility and reduced maintenance requirements.

Joint/Connection Type Analysis

The bell-and-spigot segment dominated the FRP pipe market with a 52.4% share in 2025. These joints are highly preferred because they provide strong sealing performance, easy installation, and flexibility for underground and long-distance pipelines.

They also accommodate thermal expansion and movement, reducing the risk of leakage in municipal water and industrial pipeline systems.

The butt-and-strap segment is anticipated to witness the fastest growth with a CAGR of 5.3%. These joints are widely used for custom on-site fabrication and repair work in industrial and chemical processing plants.

Their ability to create strong and permanent connections improves the structural integrity of piping systems operating under demanding conditions.

FRP Pipe Market Regional Analysis

North America FRP Pipe Market

North America accounted for the largest market share of 40.4% in 2025. Strong infrastructure rehabilitation programs, strict durability standards, and increasing adoption of corrosion-resistant materials are driving regional growth.

FRP pipes are increasingly replacing aging metallic pipelines in municipal wastewater systems, industrial facilities, and energy infrastructure because they offer superior resistance to corrosion and lower maintenance requirements.

U.S. Market Trends

The U.S. FRP pipe market reached USD 1.42 billion in 2025 and is projected to approach USD 2.75 billion by 2035, growing at a CAGR of 6.83%.

Government regulations focused on water quality, leakage reduction, and infrastructure reliability are accelerating the adoption of FRP pipes in water and wastewater systems. Strong engineering standards also support widespread acceptance of FRP materials.

Asia Pacific FRP Pipe Market

Asia Pacific is projected to grow at the fastest CAGR of 6% between 2026 and 2035. Rapid urbanization, industrial expansion, and increasing investments in water management infrastructure are major growth drivers.

Countries such as China and India are investing heavily in municipal water systems, industrial parks, wastewater treatment, and petrochemical facilities, creating significant demand for corrosion-resistant FRP piping systems.

China remains the largest market in Asia Pacific due to its massive infrastructure development programs and expanding industrial base. Growing domestic manufacturing capacity and increased use of FRP pipes in municipal and industrial projects continue to support market growth.

Europe FRP Pipe Market

Europe is experiencing steady growth due to strict environmental regulations, aging infrastructure replacement projects, and rising demand for sustainable construction materials.

FRP pipes are increasingly adopted in wastewater systems, chemical processing facilities, district energy networks, and renewable energy projects because of their durability and low maintenance needs.

Germany leads the European FRP pipe market with its advanced engineering capabilities and strict performance standards. FRP pipes are widely used in chemical plants and municipal water treatment facilities where long-term durability and corrosion resistance are critical.

Middle East & Africa FRP Pipe Market

The Middle East & Africa region is witnessing increasing FRP pipe adoption due to growing investments in desalination plants, wastewater reuse systems, and industrial infrastructure.

FRP pipes are highly suitable for harsh desert and coastal environments because they resist corrosion, scaling, and saline groundwater exposure.

South Africa is emerging as a key market in the region, supported by growing demand from mining, industrial processing, and water treatment sectors.

Government-led water infrastructure rehabilitation programs and increasing mining activities are driving the use of FRP pipes for slurry transport, acid handling, and wastewater management applications.

FRP Pipe Market Key Players

Future Pipe Industries

Large-diameter GRP/FRP pipelines and fittings (continuous filament-wound systems) for oil & gas, water, and industrial use; trenchless and open-cut installation solutions, corrosion‑resistant linings and engineered pipeline systems.

National Oilwell Varco (NOV) Inc.

Composite/fiberglass pipeline systems and flexible flowlines for oil & gas (onshore/offshore), piping components and customized composite structures for subsea, topside and process service; engineered fittings and spool fabrication.

Amiantit Group

Flowtite® FRP/GRP pipes and fittings produced with filament-winding for water, sewage, industrial and oil & gas applications; underground storage tanks and engineered system solutions including joints and coatings.

ZCL Composites Inc.

FRP composite underground storage tanks and corrosion‑resistant containment solutions, plus composite piping accessories and system components for fuel, water/wastewater and oil & gas markets.

Graphite India Limited

FRP/GRP piping and reinforced composite products for chemical processing, chlor-alkali and industrial corrosive services; custom composite vessels and linings alongside graphite-related specialty products.

Enduro Composites Inc.

Custom FRP/GRP piping, fittings, manifolds, and prefabricated composite assemblies for chemical, industrial, and corrosion‑resistant applications; engineered repair and replacement solutions.

Ershigs Inc.

Filament-wound GRP/FRP piping and fittings for industrial and municipal water and wastewater, including specialty elbows, tees, and spools for corrosive fluid handling.

Fibrex Corporation

FRP piping systems, couplings, and fittings for process industries, including pressure-rated GRP pipe, spool fabrication, and customized layups for chemical resistance.

HOBAS Pipe USA Inc.

Centrifugally cast fiberglass-reinforced polymer (CFRP/GRP) pipe systems for sewer, drainage, and pressure applications; large-diameter pipes, jacking and sliplining solutions, and accessories.

Sarplast SA

GRP/FRP piping and fittings for industrial and water applications (manufacturer of corrosion‑resistant composite pipe products and system components).

Hengrun Group Co., Ltd.

FRP/GRP pipes and fittings, often serving municipal water, drainage, and industrial markets with filament-wound or centrifugal production lines and corrosion‑resistant solutions.

Lianyungang Zhongfu Lianzhong Composites Group Co., Ltd.

Large-scale FRP/GRP pipe production (centrifugal/filament-wound) supplying water, sewage, industrial and offshore pipeline markets, including fittings and joints.

Abu Dhabi Pipe Factory

GRP/FRP pipes and fittings, typically supplied for regional municipal water, sewer, and industrial projects with engineered joint systems and corrosion protection.

FRP Systems

Tailored FRP piping systems and accessories, often providing design, fabrication, and installation support for chemical, water, and industrial applications.

Industrial Plastic Systems

Composite/FRP pipe systems, fittings, and specialty thermoplastic/FRP hybrids for corrosive process lines, municipal water and wastewater, and custom fabrication services.

Segments Covered in the Report

By Material/Type

- Polyester FRP Pipe

- Polyurethane FRP Pipe

- Epoxy FRP Pipe

- Others (Vinyl Ester, etc.)

By Application

- Oil & Gas

- Water & Wastewater

- Chemical Processing

- Power Generation

- Others (Industrial, Municipal)

By End-User

- Industrial

- Commercial

- Residential

- Others

By Joint/Connection Type

- Bell-and-Spigot

- Butt-and-Strap

- Socket-and-Spigot

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Also Read: Solder Flux Market Surges Toward USD 5.34 Billion by 2035

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/7294

You can place an order or ask any questions. Please feel free to contact us at sales@precedenceresearch.com |+1 804 441 9344