Solder Flux Market Surges Toward USD 5.34 Billion by 2035 Amid Rising Demand for Advanced Electronics Manufacturing

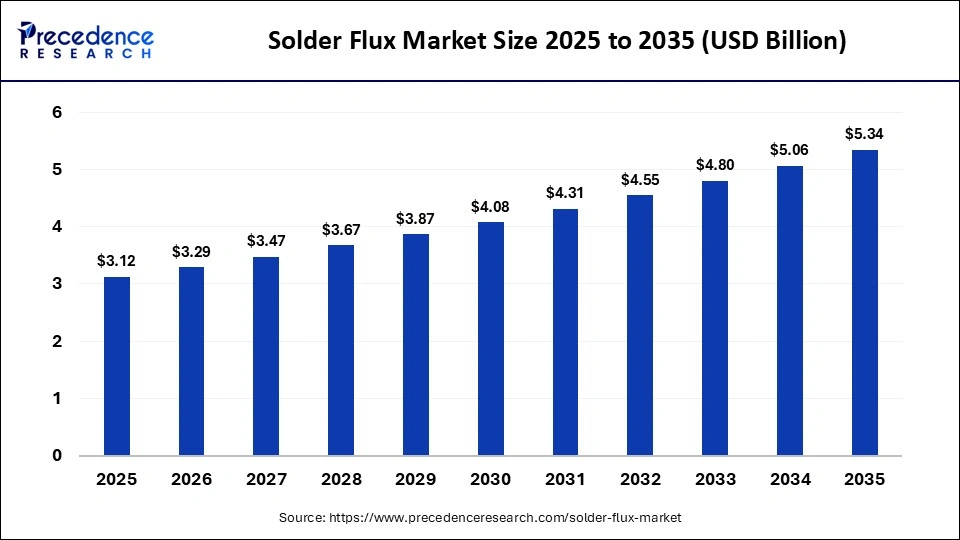

The global solder flux market is entering a transformative growth phase as electronics manufacturers increasingly prioritize high-reliability soldering, automated assembly systems, and environmentally compliant production technologies. According to Precedence Research, the market size was valued at USD 3.12 billion in 2025 and is projected to grow from USD 3.29 billion in 2026 to approximately USD 5.34 billion by 2035, registering a CAGR of 5.53% during the forecast period from 2026 to 2035.

The market is witnessing strong momentum due to the rapid expansion of consumer electronics manufacturing, increasing automotive electrification, and growing investments in telecom infrastructure and industrial automation. Solder flux, a critical material used to clean and prepare metal surfaces during soldering, has become increasingly important as electronics assemblies become smaller, denser, and more complex.

Manufacturers are also transitioning toward lead-free, halogen-free, and low-VOC formulations to comply with environmental regulations such as RoHS and REACH. At the same time, AI-powered process optimization and robotic soldering systems are reshaping soldering efficiency, enabling manufacturers to reduce defects and improve production yields.

Solder Flux Market Key Points

- The global solder flux market is expected to reach USD 5.34 billion by 2035 from USD 3.12 billion in 2025, expanding at a CAGR of 5.53% between 2026 and 2035.

- Asia Pacific dominated the global market in 2025 with a commanding 46.5% market share due to its strong electronics manufacturing ecosystem.

- North America is projected to witness the fastest growth, registering a CAGR of 6.0% during the forecast period.

- The no-clean flux segment emerged as the leading product category with a 51.7% market share in 2025 because of its low-residue and cost-saving benefits.

- Reflow soldering accounted for the largest application share of 48.7% in 2025 owing to rising miniaturization trends in electronics.

- Consumer electronics remained the largest end-use segment, contributing 42.4% of total revenue in 2025.

- Automotive electronics applications are expected to expand rapidly as EVs, ADAS, and infotainment systems continue gaining traction globally.

Solder Flux Market Revenue Outlook

| Market Indicator | Value |

|---|---|

| Market Size in 2025 | USD 3.12 Billion |

| Market Size in 2026 | USD 3.29 Billion |

| Forecast Market Size by 2035 | USD 5.34 Billion |

| CAGR (2026–2035) | 5.53% |

| Dominating Region | Asia Pacific |

| Fastest Growing Region | North America |

| Base Year | 2025 |

| Forecast Period | 2026–2035 |

How Is Artificial Intelligence Transforming the Solder Flux Market?

Artificial intelligence is increasingly becoming a key differentiator across electronics manufacturing environments, significantly influencing solder flux applications and process efficiency. AI-enabled manufacturing systems are helping companies monitor temperature profiles, solder paste behavior, flux activation windows, and conveyor speeds in real time. This level of process optimization minimizes soldering defects such as bridging, void formation, and insufficient wetting while reducing material waste and operational downtime.

AI is also enhancing robotic soldering systems and automated dispensing platforms. Machine learning algorithms can now optimize flux volume, placement precision, and dispensing speeds according to PCB layouts, component density, and solder alloy characteristics. These innovations are particularly critical for high-density PCB assemblies, fine-pitch components, micro-BGAs, and miniaturized electronics used in advanced consumer devices and automotive systems.

As manufacturers move toward Industry 4.0 production models, AI-powered soldering automation is expected to become a standard requirement across next-generation electronics assembly facilities.

What Are the Major Growth Factors Boosting the Solder Flux Market?

Rapid Expansion of Consumer Electronics Manufacturing

The growing demand for smartphones, tablets, laptops, wearable devices, gaming systems, and smart home products continues to fuel the need for reliable soldering materials. As electronics manufacturers focus on miniaturized designs and compact assemblies, advanced solder flux formulations are becoming essential for ensuring solder joint integrity and long-term product reliability.

Rising Automotive Electrification and EV Production

Electric vehicles, ADAS technologies, infotainment systems, and battery management electronics require highly reliable PCB assemblies. This trend is significantly increasing the consumption of advanced liquid and paste fluxes designed for high-temperature and fine-pitch soldering applications.

Strong Push Toward Lead-Free and Eco-Friendly Fluxes

Environmental regulations across Europe, North America, and Asia are accelerating the transition toward halogen-free, low-VOC, and lead-free soldering materials. Manufacturers are heavily investing in sustainable formulations to align with global environmental compliance standards.

Growth of Telecom Infrastructure and 5G Deployment

The rapid expansion of 5G networks and telecom infrastructure is generating higher demand for sophisticated networking hardware and communication devices. These systems require high-density PCB assemblies that rely on precise soldering performance and advanced flux chemistries.

Solder Flux Market Segment Analysis

Product Type Analysis

The no-clean flux segment dominated the solder flux market in 2025, accounting for 51.7% of the total market share. These fluxes leave minimal, non-corrosive residue after soldering, eliminating the need for post-cleaning processes. This helps manufacturers reduce production time, operational costs, and material usage. Growing demand from consumer electronics, automotive, and industrial automation sectors continues to support the adoption of advanced no-clean flux formulations.

The rosin-based flux segment is projected to expand at a CAGR of 5.2% from 2026 to 2035. Manufacturers are increasingly shifting toward rosin-based formulations because they are considered more sustainable and environmentally friendly than synthetic alternatives. Their enhanced reliability and performance in electronics assembly applications are also contributing to their rising adoption across industries.

Application/Soldering Process Analysis

The reflow soldering segment held the largest market share of 48.7% in 2025. The segment’s growth is mainly driven by increasing miniaturization in electronics, rising IoT and 5G adoption, and rapid automotive electrification. Demand for reliable and energy-efficient soldering solutions across automotive, aerospace, and consumer electronics industries is further strengthening the segment.

The selective soldering segment is expected to witness a CAGR of 5.25% during the forecast period. Rising demand for high-reliability electronics in electric vehicles, ADAS systems, aerospace, and defense sectors is accelerating growth. Increasing automation and Industry 4.0 integration are also encouraging the adoption of selective soldering technologies.

Form Analysis

The liquid flux segment accounted for 42.5% of the market share in 2025. Liquid fluxes are widely used in automated, high-volume manufacturing environments because they provide uniform coverage and controlled activation. Their low viscosity supports precise application on densely populated PCBs, helping manufacturers reduce defects and improve soldering consistency.

The paste flux segment is expected to grow at a CAGR of 5.1% over the forecast period. Increasing use of surface mount technology (SMT), fine-pitch components, and advanced electronic packaging is driving demand for paste fluxes. Their controlled rheology allows accurate stencil printing and dispensing, making them ideal for miniaturized electronic assemblies.

End-Use Industry Analysis

The consumer electronics segment led the solder flux market with a 42.4% share in 2025. Continuous demand for smartphones, tablets, wearables, and smart devices is increasing the need for reliable soldering solutions for compact electronic components. Growing adoption of AI, IoT, and connected technologies is further boosting market demand.

The automotive segment is projected to grow at a CAGR of 5.3% from 2026 to 2035. Increasing production of electric vehicles, infotainment systems, and ADAS technologies is creating strong demand for high-performance soldering materials. Miniaturization trends and strict environmental regulations are also contributing to market growth.

Solder Flux Market Regional Analysis

Why Does Asia Pacific Dominate the Solder Flux Market?

Asia Pacific dominated the global solder flux market in 2025 due to its large-scale electronics manufacturing base and strong demand for consumer electronics. Countries such as China, Japan, South Korea, and Taiwan remain major hubs for semiconductor and PCB production. Government initiatives supporting domestic electronics manufacturing and increasing adoption of eco-friendly soldering materials are further driving regional growth.

China remains a major contributor to the market because of rapid industrialization, high electronics production, and increasing automation in manufacturing. Government initiatives like “Made in China 2025” and the transition toward lead-free soldering technologies are accelerating market expansion. Rising demand for smartphones, PCs, and other electronic devices continues to support flux consumption.

North America Insights

North America is emerging as the fastest-growing market due to rapid adoption of IoT, AI, and Industry 4.0 technologies in electronics manufacturing. Manufacturers are upgrading SMT and selective soldering systems, increasing demand for advanced flux solutions. Stringent environmental regulations are also encouraging the use of low-VOC, halogen-free, and lead-free flux formulations.

The U.S. solder flux market is expanding because of rising industrial automation and strong demand from automotive, telecommunications, and consumer electronics industries. Increasing production of EVs, telecom infrastructure, and compact electronic devices is driving the need for high-performance soldering materials compatible with fine-pitch PCB assemblies.

Europe Insights

Europe holds a significant share of the market due to increasing investment in industrial automation and 5G infrastructure. Electronics manufacturers are adopting advanced SMT and selective soldering technologies to improve product reliability. Strict EU environmental regulations are also acceerating the transition toward lead-free and halogen-free soldering solutions.

Germany is witnessing strong market growth because of increasing electronics integration in electric vehicles and advanced driver-assistance systems. Demand for reliable soldering in automotive electronics, telecom equipment, and industrial communication systems is boosting the adoption of advanced liquid and paste fluxes.

Middle East & Africa Insights

The Middle East & Africa market is growing steadily due to rising industrialization and increasing demand for consumer electronics and IoT devices. Government-led smart city projects in countries such as the UAE and Saudi Arabia are increasing the adoption of advanced electronic systems, driving demand for solder flux products.

South Africa is experiencing notable market growth due to expanding industrial activities, increasing investment in smart infrastructure, and growing adoption of industrial automation. Rising demand for automotive electronics and consumer devices is further supporting the need for reliable soldering materials and high-quality PCB assembly solutions.

Top Companies in the Solder Flux Market

Henkel AG & Co. KGaA

Kester (Illinois Tool Works Inc.)

Alpha Assembly Solutions

Indium Corporation

AIM Solder

Senju Metal Industry Co., Ltd.

Heraeus Holding GmbH

Shenmao Technology Inc.

Tamura Corporation

Inventec Performance Chemicals

KOKI Company Ltd.

Balver Zinn Josef Jost GmbH & Co. KG

Superior Flux & Mfg. Co.

MG Chemicals

Nordson Corporation

Segments Covered in the Report

By Product Type

- No-Clean Flux

- Rosin-Based Flux

- Water-Soluble Flux

- Synthetic Flux

By Application/Soldering Process

- Reflow Soldering

- Wave Soldering

- Selective Soldering

- Hand Soldering

By Form

- Liquid Flux

- Paste Flux

- Gel Flux

- Solid Flux

By End-Use Industry

- Consumer Electronics

- Automotive

- Industrial Electronics

- Aerospace & Defense

- Telecommunications

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Read Also: 3D Printing Photopolymers Market Surges Toward USD 5.56 Billion by 2035

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/7299

You can place an order or ask any questions. Please feel free to contact us at sales@precedenceresearch.com |+1 804 441 9344